Preparing for HYDROGEN HORIZONS 2025 conference organised by The Voice of Renewables Events (VOR events), held this year on November 12th, 2025 in Vilnius, Lithuania, website: https://vorevents.com/h2/, we wrote a concise summary of hydrogen and P2X landscape in Poland:

As Europe races toward decarbonisation and energy independence, Poland finds itself at a pivotal moment – transitioning from a coal-reliant energy mix to a more sustainable, diversified future. Among the most promising pathways emerging is the development of a robust hydrogen economy and Power-to-X (P2X) technologies, which together could redefine the country’s energy landscape over the next two decades.

Hydrogen, particularly green hydrogen produced via electrolysis using renewable energy, is increasingly viewed as a strategic solution to decarbonize hard-to-abate sectors such as heavy industry, transport, and heating. Complementing this, P2X technologies – which convert electricity into fuels, chemicals, or heat – offer a way to store surplus renewable energy and create synthetic alternatives to fossil-based resources. For Poland, these innovations could be key to aligning with EU climate targets while enhancing energy security and industrial competitiveness.

Key Challenges on the Road Ahead

Despite its growing ambitions, Poland faces a range of structural, technical, and regulatory challenges in scaling up hydrogen and Power-to-X (P2X) technologies.

1. Heavy Coal Dependence and Energy Transition Pace

Poland remains one of the most coal-dependent countries in Europe, with coal still accounting for over 60% of its electricity generation. This reliance slows the integration of renewables, which are essential for producing green hydrogen and powering P2X processes. While the government has outlined plans to phase out coal, the pace of transition remains constrained by political sensitivities, legacy infrastructure, and the social impact on mining regions.

2. Underdeveloped Renewable Capacity

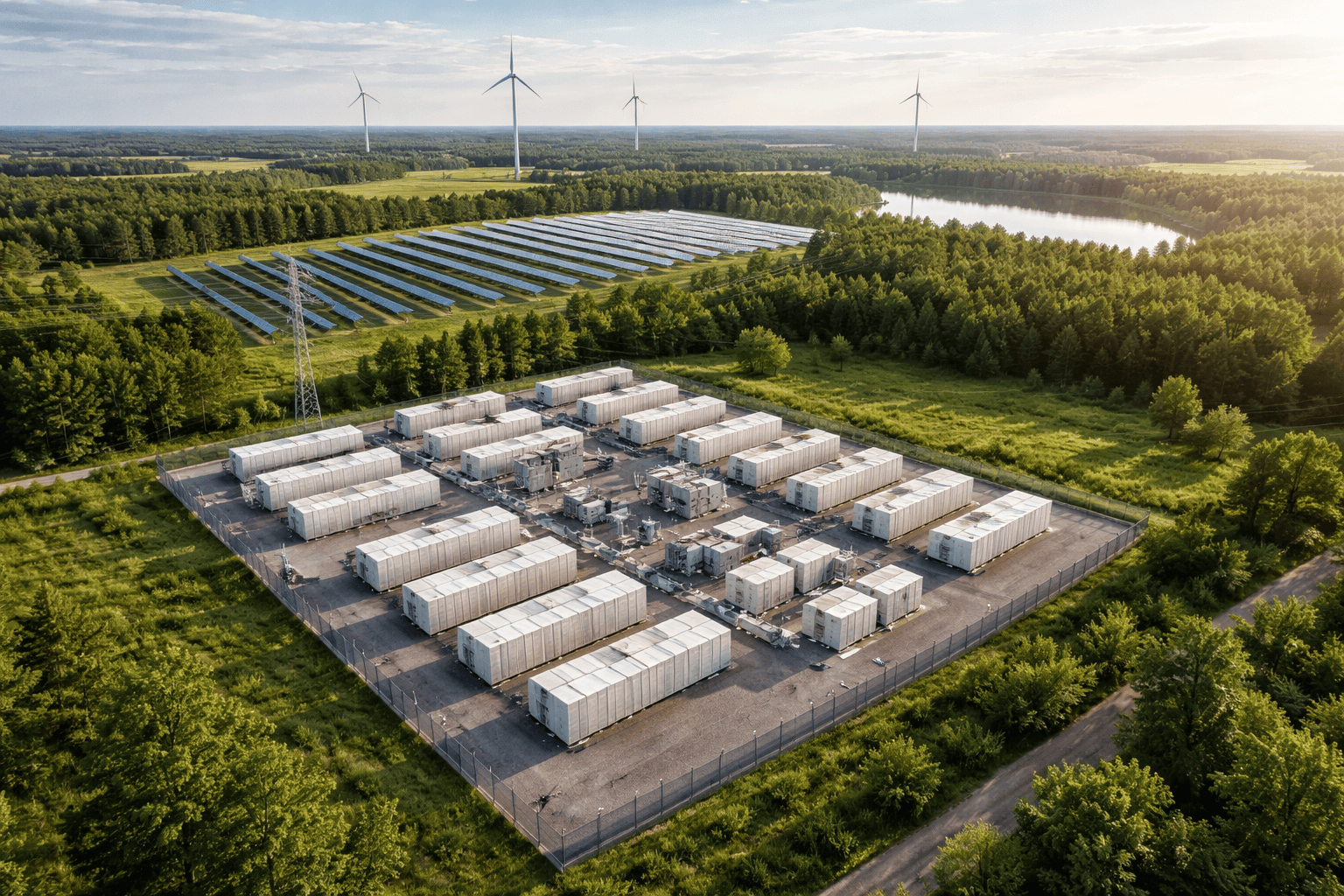

Although Poland has made progress in wind and solar, its renewable capacity is still insufficient to support large-scale green hydrogen production. Offshore wind – critical to the future hydrogen supply chain – is only now gaining momentum, and onshore wind continues to face permitting and spatial planning challenges. Without a significant and rapid buildout of clean energy, the production of truly low-emission hydrogen will remain limited.

3. Regulatory Uncertainty and Delayed Frameworks

Poland lacks a comprehensive, binding legal and regulatory framework for hydrogen and P2X deployment. While a national hydrogen strategy has been introduced, concrete legislation around hydrogen certification, infrastructure development, safety standards, and market incentives is still in early stages. This uncertainty hampers investment and long-term planning for both domestic and international stakeholders.

4. Infrastructure Gaps and Grid Limitations

The development of hydrogen production and distribution infrastructure – such as pipelines, storage facilities, refuelling stations, and electrolyser networks – is still nascent. Additionally, Poland’s electricity grid will need modernization and reinforcement to handle increased loads from electrification and renewable integration, which are foundational for P2X viability.

5. High Costs and Economic Viability

Green hydrogen and P2X technologies are still more expensive than fossil-based alternatives. Without strong financial incentives, carbon pricing mechanisms, or subsidies, project developers face difficulties in making large-scale investments bankable. This is especially relevant in energy-intensive sectors where margins are tight and the cost gap between conventional fuels and hydrogen-based alternatives remains significant.

6. Limited R&D and Workforce Expertise

While Poland has strong engineering and industrial capabilities, dedicated research and development in hydrogen and P2X technologies is still in early stages. Building a skilled workforce, fostering academic-industry collaboration, and scaling innovation will be critical for long-term competitiveness in this evolving sector.

Strategic Opportunities for Poland

While the road to a hydrogen and Power-to-X (P2X) future is complex, Poland holds several strategic advantages that could position it as a key player in Europe’s emerging clean energy ecosystem.

1. Leveraging Industrial Strength and Geographic Position

Poland’s well-established industrial base – particularly in chemicals, steel, refining, and heavy manufacturing – makes it a natural candidate for early hydrogen adoption. Many of these sectors are difficult to decarbonise using electricity alone and are ideally suited for hydrogen-based solutions. Moreover, Poland’s central location in Europe allows it to act as a hydrogen corridor between Western Europe and Eastern markets, potentially serving as a regional hub for hydrogen production, storage, and transport.

2. Offshore Wind as a Green Hydrogen Backbone

The Baltic Sea presents a major untapped resource for offshore wind development, which can serve as the backbone for green hydrogen production. With ambitious offshore wind targets (up to 11 GW by 2040), Poland has the potential to co-locate large-scale electrolysers near future wind farms, enabling direct conversion of wind power into clean hydrogen and synthetic fuels – essential for scalable P2X applications.

3. EU Funding and Policy Alignment

Poland stands to benefit from significant EU support through instruments like the Innovation Fund, REPowerEU, and the Connecting Europe Facility. These funds can accelerate the deployment of hydrogen valleys, research initiatives, and cross-border infrastructure projects. By aligning national strategies with broader EU climate and energy goals, Poland can secure financial backing while integrating into the continent’s hydrogen backbone.

4. Domestic Demand and Export Potential

With high domestic demand potential in heavy transport, aviation, fertilizers, and power generation, Poland has ample use cases to build a domestic hydrogen economy. At the same time, as Western Europe scales up hydrogen imports, Poland can become a key supplier and transit country – particularly if it invests early in cross-border pipelines and storage facilities.

5. Development of Hydrogen Valleys

Poland is already exploring regional “hydrogen valleys” – localised ecosystems where hydrogen production, distribution, and consumption are co-located. These projects, supported by both national and EU funding, offer scalable models that reduce transport costs, create local jobs, and build early market momentum. Successful implementation could pave the way for broader deployment across the country.

6. Innovation and Technological Leadership

By investing in R&D and fostering public-private partnerships, Poland has the chance to become a leader in specific hydrogen and P2X technologies such as high-temperature electrolysis, hydrogen-ready turbines, and synthetic fuel production. Building this innovation ecosystem now can help create exportable technologies and expertise in a market poised for exponential growth.

Polish Government Strategy & Ministerial Initiatives

- Polish Hydrogen Strategy to 2030 (with 2040 outlook): Launched in 2021, this comprehensive plan sets ambitious targets across the hydrogen value chain:

- Production: Reach 2 GW of installed low-carbon hydrogen capacity by 2030, enabling synthetic gas production and ammonia usage; electric‑based hydrogen fuels industrial and mobility applications.

- Mobility: Roll out 100–250 hydrogen buses and 32 refuelling stations by 2025; expand to 800–1,000 buses by 2030, alongside infrastructure for trains, maritime, synthetic fuels.

- Industry & Hydrogen Valleys: Develop at least five “hydrogen valleys” (regional clusters integrating production, research, transport, consumption) by 2030.

- Energy Sector & P2X: Pilot 1 MW power‑to‑gas (P2G) systems by 2025 and deploy cogeneration/polygeneration up to 50 MW by 2030; assess inclusion of synthetic gases into gas networks, including a North–South hydrogen pipeline feasibility study.

- Regulatory Framework: Finalize a hydrogen legislative package by 2022–2023, covering market operations, incentives, and EU law alignment.

- Investment Support: Invest approximately PLN 930 million by 2025 and PLN 1.8 billion by 2030 in hydrogen public transport; exceed PLN 9 billion in electrolysers by 2030 – combined, over PLN 11 billion.

- Subsidies & Funding: From December 2024, the government launched a €640 million subsidy program (≈€2 million per MW) for hydrogen production projects (≥20 MW). By July 2025, around PLN 2.7 billion was allocated to six hydrogen-production facilities via the National Recovery and Resilience Facility, including Orlen’s “Hydrogen Eagle” and “Green H₂” projects.

GAZ‑SYSTEM’s Role in Infrastructure

- Hydrogen Market Mapping: In 2024, GAZ‑SYSTEM conducted a landmark survey – the Hydrogen Map of Poland – covering 178 complete projects across production, consumption, distribution, and storage. It forecasted domestic production stabilizing at 1.11 Mt/year by 2040, while demand could reach 2.62 Mt by 2040, implying reliance on imports of 0.8–1.4 Mt. The study also highlighted major infrastructure gaps – especially in transmission and storage -and called for creation of a National Hydrogen Network and hydrogen hubs.

- Legal Operator Status: In June 2025, GAZ‑SYSTEM became the official hydrogen transmission network operator (HTNO) in Poland until at least August 2026, per Energy Law amendments.

- EU-Funded Projects & Studies:

- Nordic–Baltic Hydrogen Corridor: GAZ‑SYSTEM submitted this as a Project of Common Interest (PCI), which aims to connect Finland, Baltic States, Poland, and Germany with hydrogen infrastructure.

- Pomeranian Green H₂ Cluster: Secured €190 000 EU funding for feasibility studies assessing green hydrogen generation and cross-border infrastructure in NW Poland in collaboration with German partners.

- Pilot Studies & Horizon Projects: Since 2023, GAZ‑SYSTEM has collaborated on EU-funded projects (THOTH2 and SHIMMER) developing metering, safety standards, and modelling for hydrogen–gas mixtures and network resilience.

Noteworthy Projects and Implementation on the Ground

- Hydrogen Valleys in Action:

- Central Hydrogen Valley (Kielce): Focused on 250 MW hydrogen production, it integrates logistics, transport, energy, academia, and tech firms.

- Lower Silesian Hydrogen Valley: A cross-border consortium with Baltic region partners building a full hydrogen value chain.

- Orlen’s Initiatives:

- H₂ Academy & Mobility: Educational programs for hydrogen specialists launched in 2023. Poland’s first hydrogen locomotive is in operation; Orlen is also expanding hydrogen bus fleets and refuelling stations—by 2030 aiming for 57 stations in Poland, plus outlets in Czechia and Slovakia.

- HySpark Project: Funded with €9 million by the EU’s Clean Hydrogen Partnership, this aims to deploy hydrogen-powered vehicles and a refuelling station at Chopin Airport by 2026.

- Early Infrastructure Deployment: In mid‑2024, Orlen launched Poland’s first public hydrogen refuelling station in Poznań, followed by a second in Katowice.

Outlook: Toward a Hydrogen & P2X Future

Outlook: Toward a Hydrogen & P2X Future

- Scaling Up Production & Funding

Strong public funding – via subsidies, Recovery Plan, EU programs – enables rapid build-out of electrolysers, hydrogen valleys, and synthetic fuel operations. - Building the Transmission Backbone

GAZ‑SYSTEM, now HTNO, is spearheading infrastructure planning, feasibility studies, pilot projects, and legal frameworks to ensure a cohesive national hydrogen network. - Local Implementation & Ecosystems

Hydrogen valleys and pilot clusters offer region-specific models for scaling up production, use, and innovation, with diverse stakeholders collaborating. - Mobility & Energy Integration

Widespread deployment of buses, trains, airport vehicles, and public refuelling stations will catalyse demand. Parallel investments in P2G, storage, and blending into gas networks expand utility and resilience. - Regulatory & Market Foundations

Legislative frameworks and market incentives – including auctions, CfD models, EU-level advocacy for fairness – lay the groundwork for sustained growth in hydrogen and P2X.

Summary

Poland’s future hydrogen and P2X development hinges on strategic alignment between:

- Ministry-driven targets and incentives, pushing production, regulatory clarity, infrastructure planning.

- GAZ‑SYSTEM’s execution, building market mapping, infrastructure readiness, and cross-border connectivity.

- Industry & local pilots, turning strategy into real-world deployment across energy, transport, and industrial sectors.

Together, these actions map a bold roadmap for Poland to become a key hydrogen and P2X hub in Europe by 2030 and beyond.

Detailed Look at Poland’s Hydrogen Valley Initiatives

Poland’s hydrogen valley strategy demonstrates a comprehensive, multi-regional rollout of hydrogen ecosystems – spanning heavy industry, mobility, energy, and research across all major zones. Each valley is designed to be a self-contained innovation and production hub, tailored to local strengths and global climate goals.

Drawing from the Ministry of Energy, ARP (Industrial Development Agency), and other authoritative sources, here’s a breakdown of key hydrogen valley projects currently shaping Poland’s hydrogen economy:

1. Central Hydrogen Valley (Świętokrzyskie – Łódzkie – Podkarpackie – Mazowieckie)

- Headquarters: Kielce

- Stakeholders: Industria Group, ENEA, ML System, Łódź SEZ, Rolls‑Royce SMR, Świętokrzyska University of Technology, ARP, GAZ‑SYSTEM, local governments, and others.

- Capacity & Focus: Up to 250 MW of electrolyser capacity. Emphasis on clean hydrogen production, decarbonizing logistics, public and rail transport, and exploring hydrogen production via nuclear energy.

- Status: Advanced into feasibility and early development stages, with strong multi-sector collaboration.

2. Lower Silesian Hydrogen Valley

- Headquarters: Wrocław

- Stakeholders: KGHM, Grupa Azoty, Toyota Motor Poland, Total Energies, Linde, Wrocław universities, ARP, GAZ‑SYSTEM, and regional authorities.

- Capacity & Focus: Aims at 1,700 t H₂/year. Specializes in hydrogen storage, trigeneration, green copper and metallurgical applications, river transport (hydrogen barges on the Oder), agro-voltaics, and cross-border innovation ecosystems.

- Status: Officially established in February 2022 via ARP initiative. A Letter of Intent also marks cross‑border R&D cooperation with European partners from Saxony, Brandenburg, and the Czech Moravian‑Silesian region.

3. Masovian (Mazovian) Hydrogen Valley

- Headquarters: Płock

- Stakeholders: PKN Orlen, ARP, BGK, Toyota Motor Europe, Siemens Energy, Warsaw and AGH universities, Energy Institute, national agencies, and GAZ‑SYSTEM.

- Focus: Integration within petrochemical value chains, synthetic fuel production, CO₂ capture, hydrogen logistics, public and rail transport (hydrogen buses and locomotives), and green chemistry.

- Status: Letter of Intent signed involving 25 entities; cluster development currently underway, slated for establishment by Q1 2022.

4. Silesia–Lesser Poland (Śląsko‑Małopolska) Hydrogen Valley

- Headquarters: Katowice

- Stakeholders: Orlen Południe, Polenergia, ARP, JSW Innovation, Azoty Tarnów, universities (Silesian, AGH), KOMAG, local governments.

- Focus: Green glycol manufacturing, green steel production, low-carbon hydrogen supply, and decarbonization of public transportation.

- Status: Formally organized as an association, actively rolling out projects in energy transformation.

5. Subcarpathian (Podkarpacka) Hydrogen Valley

- Headquarters: Rzeszów

- Stakeholders: Rzeszów University of Technology, Polenergia, Autosan, ML System, Marshal’s Office, ARP, aviation Valley enterprises.

- Focus: Zero‑emission hydrogen production (~5 MW electrolyser capacity), hydrogen-powered buses, aviation applications, green heating and power, and regional energy integration.

- Status: Active development stage; project development assistance submitted .

6. Pomeranian (Baltic) Hydrogen Valley

- Headquarters: Gdańsk

- Stakeholders: Pomeranian Marshal’s Office, Hydrogen Technology Cluster, Gdańsk University of Technology, port authorities, Sescom, PKP Energetyka.

- Focus: Public transport decarbonization, hydrogen from offshore renewables, port decarbonization, hydrogen storage, and electrolyzer production.

- Status: Initial regional mapping and cluster formation underway.

7. Greater Poland (Wielkopolska) Hydrogen Valley

- Headquarters: Poznań

- Stakeholders: Wielkopolska Marshal’s Office, ZE PAK, Solaris, Adam Mickiewicz University, Poznań University of Technology, local municipalities, and the airport.

- Focus: Electrolyzer capacity (~10 MW), hydrogen for housing, air transport (Poznań Airport), public transport, and power generation.

- Status: Advisory board established; regional needs mapped; promotional portal launched.

8. West Pomeranian Hydrogen Valley

- Headquarters: Szczecin

- Stakeholders: West Pomeranian University of Technology, Azoty Police, ARP, Enea, port authorities, universities (Koszalin, Maritime).

- Focus: Green ammonia, low-emission maritime and river transport, ammonia import infrastructure, offshore hydrogen production.

- Status: Association forming; over 30 entities interested.

Summary Table

| Valley | HQ | Stakeholders & Focus |

| Central | Kielce | Clean H₂, transport, nuclear, logistics |

| Lower Silesian | Wrocław | Green metallurgy, storage, river transport, innovation, cross-border |

| Masovian | Płock | Petrochemicals, synthetic fuels, rail, green chemistry |

| Silesia–Lesser Poland | Katowice | Green steel, glycol, public transport, decarbonization |

| Subcarpathian | Rzeszów | Hydrogen buses, aviation, energy, heating |

| Pomeranian | Gdańsk | Port hydrogen, offshore renewables, electronics, storage |

| Greater Poland | Poznań | Housing, airport, public transport, power |

| West Pomeranian | Szczecin | Green ammonia, maritime, import infrastructure, offshore |

Conclusion

Poland stands at a crossroads in its energy transition – facing the urgent need to move beyond coal while unlocking the economic and environmental potential of a clean energy future. Hydrogen and Power-to-X technologies offer a compelling pathway, not only for decarbonizing industry and transport but also for securing long-term energy resilience and aligning with EU climate targets.

While significant challenges remain – from regulatory delays to infrastructure gaps – Poland’s industrial base, geographical position, and renewable energy potential provide a solid foundation for success. By accelerating investment, clarifying policy frameworks, and leveraging EU support, Poland can position itself not just as a hydrogen adopter, but as a regional leader and exporter in the emerging hydrogen economy.

The coming years will be critical. Strategic choices made now – on regulation, innovation, and infrastructure – will shape Poland’s role in Europe’s decarbonized energy landscape for decades to come.

HYDROGEN HORIZONS 2025 conference, organised by The Voice of Renewables and sponsored by leading consultancy Renwise, will be held on November 12th, 2025 in Vilnius, Lithuania.

Event website: https://vorevents.com/h2/

Register: https://buy.stripe.com/6oUeVc4M74FxcFvaYQffy1h

Read this article on LinkedIn: https://www.linkedin.com/pulse/polands-path-toward-hydrogen-p2x-future-voiceofrenewables-hhhae