Chile’s energy transition in 2026 is no longer defined by questions of ambition, resource availability or even technology cost. Those debates have largely been resolved in favour of a clear trajectory toward deep decarbonisation, electrification and long-term carbon neutrality. Instead, the defining issue has become whether the country can translate its exceptional renewable resource base into a fully integrated energy system capable of supporting sustained industrial competitiveness, stable investment conditions and long-term economic value creation. Across developers, utilities, transmission operators, mining companies, hydrogen developers and institutional investors, there is now broad alignment on direction, but increasing divergence on execution.

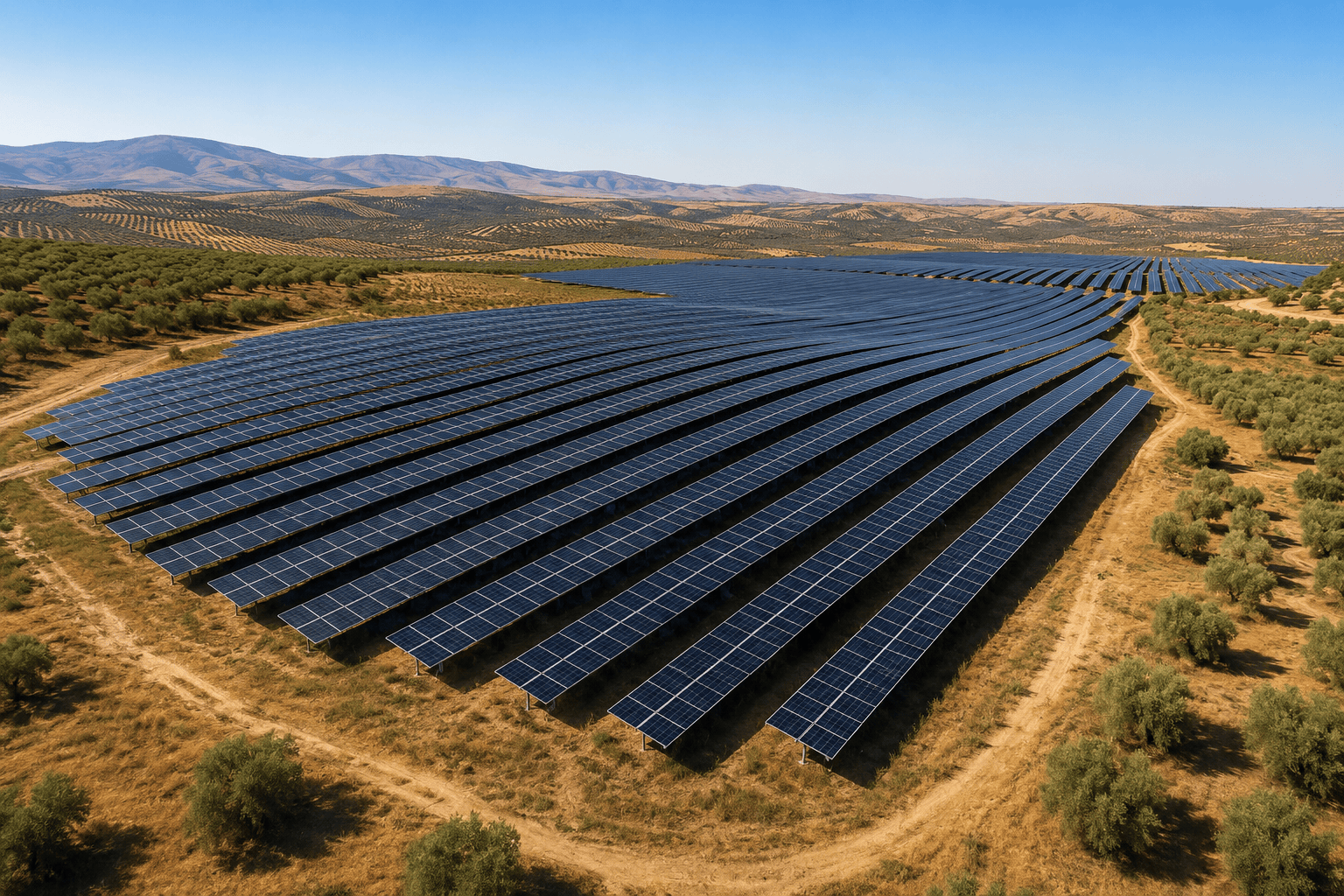

Over the past decade, Chile has established itself as one of the world’s most advanced renewable energy markets, underpinned by world-class solar irradiation in the Atacama Desert and strong wind resources in the south. However, the system that connects generation to demand has not evolved at the same pace as installed capacity. As a result, the country is increasingly experiencing structural congestion, curtailment in high-resource zones, and delays in project monetisation. This reflects a fundamental shift: Chile is no longer constrained by renewable supply, but by the ability of its transmission, storage and demand systems to absorb and utilise that supply efficiently.

Transmission as the Chilean electricity system backbone

Transmission has moved from a supporting engineering function to the principal structural constraint of Chile’s electricity system, and therefore the decisive determinant of renewable value realisation. The rapid build-out of variable solar and wind capacity in resource-rich but geographically remote regions—particularly the Atacama and northern mining corridors—has fundamentally decoupled generation growth from transmission expansion. As a result, the system is no longer generation-constrained, but transfer-constrained, with congestion increasingly dictating realised prices, curtailment levels and investment returns.

This dynamic is most visible in persistent north–centre bottlenecks, where surplus daytime solar generation frequently coincides with transmission saturation, forcing curtailment or deep price cannibalisation. In such conditions, the marginal value of new renewable capacity is no longer determined by resource quality alone, but by its access to evacuation capacity. Transmission scarcity has therefore become a de facto pricing mechanism within the Chilean power market, redistributing value between unconstrained and constrained nodes.

The most emblematic response to this structural imbalance is the Kimal–Lo Aguirre high-voltage direct current (HVDC) transmission line, a multi-billion-dollar infrastructure project widely estimated at around US$1.5 billion. Designed to link the northern generation hub with the central consumption load centre around Santiago, the project represents a step-change in system architecture rather than incremental grid reinforcement. By enabling bulk transfer of low-cost solar generation from the Atacama to mining operations, urban demand centres and emerging industrial loads, it directly addresses the spatial mismatch between supply and demand.

Crucially, Kimal–Lo Aguirre should be understood not merely as a transmission asset, but as an enabling platform for the re-pricing of Chile’s entire electricity system. It effectively unlocks latent renewable value currently suppressed by congestion, while simultaneously reshaping investment logic across generation, storage and large-load electrification. In this sense, transmission is no longer a passive conduit for electrons, but the backbone of system-wide value creation—determining where capital is allocated, which projects are bankable, and how Chile’s energy transition translates into industrial competitiveness.

At a broader level, this shift elevates transmission infrastructure into a macroeconomic variable. It connects Chile’s mining-intensive export model with its renewable resource endowment, effectively integrating energy geography with industrial geography. The implication is clear: future competitiveness in Chile’s energy system will depend less on installed renewable capacity and more on the speed, scale and regulatory efficiency of transmission deployment.

Mining as the structural anchor of demand

At the same time, the demand side of the system is undergoing a profound transformation. Electrification is no longer incremental but structural, driven by mining, heavy industry, urban systems and an emerging layer of digital infrastructure. Mining in particular has become the central structural anchor of Chile’s energy system. As the world’s largest copper producer and a major lithium supplier, Chile sits at the centre of global electrification supply chains. This position is increasingly translating into long-term contracted demand for renewable electricity, with companies such as Codelco, BHP, Antofagasta Minerals and Anglo American entering multi-decade power purchase agreements to secure low-carbon energy supply.

This mining-driven demand base is not only large but highly system-relevant. It provides long-duration, creditworthy electricity offtake that underpins investment in generation, transmission and storage assets. In practical terms, mining is now functioning as a quasi-baseload demand anchor in a system dominated by variable renewable generation. This is also reshaping project economics, as developers increasingly rely on mining-linked PPAs to secure financing for large-scale renewable and hybrid projects.

Hybrid renewables and the rise of storage-led systems in Chile

This dynamic is most visibly expressed in the rapid emergence of hybrid renewable and storage systems across Chile, which are fundamentally reshaping how renewable energy projects are being conceived, financed and operated. Rather than functioning as incremental additions to existing solar and wind assets, battery storage is now becoming the defining component of new project architectures, effectively shifting the investment logic from energy generation to system firming and dispatch optimisation.

A key driver of this shift is the increasing economic cost of system constraints. Rising curtailment in northern Chile, driven by transmission bottlenecks and temporal mismatches between peak solar generation and demand centres, has created a structural need for storage not simply as a flexibility tool, but as a revenue protection mechanism. In parallel, price volatility across Chile’s nodal electricity market has increased the arbitrage value of time-shifting renewable output, while tightening reserve margins have elevated the value of capacity-like system contributions. Together, these factors are effectively converting storage from a marginal enhancement into a core asset class within the power system.

This is reflected in the scale and structure of emerging projects. AES Andes is advancing a portfolio including the Pampas and Cristales developments in northern Chile, combining approximately 1,325 MW of renewable generation with around 2.2 GWh of battery storage, underpinned by an estimated investment of roughly US$1.1 billion. Importantly, these projects are not designed as standalone generation assets, but as integrated energy systems explicitly structured to mitigate curtailment risk and improve dispatchability in congested grid zones. In doing so, they reflect a broader redefinition of renewable project economics, where value is increasingly determined by system contribution rather than energy output alone.

A similar pattern is evident in Generadora Metropolitana’s Dune Plus project, which adds approximately 509 MW of renewable capacity alongside more than 2 GWh of storage, supported by long-term supply arrangements linked to mining demand, including exposure to Codelco. The significance of this structure lies not only in its scale, but in its contractual logic: storage is effectively being monetised through industrial offtake stability, transforming mining-linked demand into a de facto system anchor for firmed renewable capacity.

Collectively, these developments illustrate a structural transition in Chile’s power sector architecture. Storage is no longer being deployed as a balancing tool within a conventional energy-only market framework, but as a core enabler of a hybrid system in which generation, flexibility and capacity are increasingly bundled into single investment structures. This represents an important shift in market design: Chile is gradually evolving toward a system in which value is derived not solely from megawatt-hours produced, but from the ability to deliver firm, dispatchable and geographically deliverable energy to constrained demand centres.

In this context, hybrid renewable and storage systems are not simply a technological evolution, but an institutional response to a deeper structural constraint — the mismatch between geographically concentrated renewable supply and increasingly complex, spatially distributed industrial demand. As a result, storage is moving from optional infrastructure to a foundational component of Chile’s emerging energy system architecture.

Chilean hydrogen industry and industrial decarbonisation

The same system logic is now extending into hydrogen development. Chile’s hydrogen strategy is moving decisively from an export-led narrative toward execution and industrial anchoring. While green ammonia and synthetic fuels remain central to long-term export ambitions, the most credible near-term demand signals are increasingly domestic. The most significant example of capital deployment in this space is the proposed TotalEnergies green hydrogen and ammonia project in the Magallanes region, with an estimated investment of approximately US$16 billion. The project integrates large-scale wind generation, electrolysis capacity, ammonia production and export infrastructure, representing one of the largest hydrogen developments globally.

However, beyond export potential, hydrogen is increasingly being viewed through the lens of domestic industrial decarbonisation, particularly in mining operations, where it is being explored for haul truck fleets, remote site energy systems and high-temperature industrial processes. This shift is important because it signals a structural evolution in hydrogen’s role within Chile’s energy system. Rather than functioning purely as an export commodity, hydrogen is becoming a dual-purpose infrastructure layer embedded within industrial systems.

Emerging energy demand re-architecture: Chilean cities, industry and data infrastructure demand re-architecture

At the same time, Chile’s electricity demand structure is undergoing a fundamental reconfiguration rather than simple expansion. The system is transitioning from a relatively linear model of industrial and residential load growth to a multi-layered demand architecture shaped by electrification, digitalisation and industrial decarbonisation occurring simultaneously. This shift is as consequential for system design as the expansion of renewable generation itself, as it alters not only total demand volumes but also load shape, geographic concentration and temporal predictability.

Beyond mining electrification, which remains the dominant structural driver of industrial demand, urban expansion and transport electrification are steadily increasing baseline consumption in metropolitan areas, particularly around Santiago and other major population centres. However, the most significant structural change is emerging in the form of digital infrastructure, particularly data centres, hyperscale computing facilities and cloud service platforms. Unlike traditional industrial loads, these assets exhibit continuous, high-utilisation demand profiles with minimal load variability, effectively introducing a new category of “always-on” electricity consumption into the system.

This development is strategically important because data infrastructure behaves more like industrial baseload than conventional commercial demand, while also being highly sensitive to grid reliability, latency and regional energy pricing. As global digitalisation accelerates, Chile is increasingly positioned as a potential regional node for data infrastructure, reinforcing the need for highly reliable, low-carbon and geographically stable electricity supply. This creates a structurally new demand class that is both energy-intensive and system-sensitive, increasing the importance of transmission stability and real-time system balancing.

When combined with industrial electrification in mining and manufacturing, as well as urban transport decarbonisation, these trends are producing a more fragmented and spatially distributed demand system. Unlike historical demand growth, which was relatively predictable and geographically concentrated, future demand is increasingly multi-nodal, spanning mining corridors in the north, urban centres in central Chile, and emerging digital and industrial clusters across multiple regions. This evolution significantly increases the complexity of transmission planning and elevates the importance of system flexibility, particularly storage and demand response.

In parallel, energy efficiency and demand-side optimisation are becoming central structural components of this transformation rather than marginal improvements. The National Association of Energy Efficiency Companies (ANESCO Chile) has emphasised that energy efficiency is increasingly functioning as a competitiveness lever rather than solely a cost-reduction mechanism. In energy-intensive sectors such as mining, metals processing and advanced manufacturing, improvements in energy productivity are directly linked to international competitiveness, while also enabling deeper penetration of variable renewable energy into industrial operations.

More broadly, this reflects a systemic shift in how energy demand interacts with industrial strategy. Electrification, efficiency, and digitalisation are no longer separate policy or technology trends, but interdependent forces shaping a new demand architecture in which industrial competitiveness is increasingly determined by access to flexible, reliable and low-carbon electricity rather than energy cost alone.

Investment logic shift and regulatory context

From an investment perspective, these structural shifts are fundamentally changing decision-making frameworks. Where investment decisions were previously driven primarily by resource quality, capacity factors and levelised cost of energy, they are now increasingly shaped by system integration constraints. Transmission access, permitting timelines, offtake structure, storage requirements and execution risk have become central determinants of project viability. Chile remains one of the most attractive renewable energy markets globally, but it is now competing not only on natural resource endowment but on its ability to deliver complex, integrated infrastructure systems at scale.

Recent regulatory reforms, including the 2025 Sectoral Authorisations Framework Law (LMAS), represent an important step toward addressing permitting fragmentation and improving execution efficiency. However, regulatory reform alone does not resolve the underlying challenge of system complexity. Execution capability — across transmission, storage, generation and industrial integration — remains the primary constraint shaping investment outcomes.

Conclusion: from energy market to industrial system

Taken together, these dynamics define a structural transition in Chile’s energy system. The country has moved beyond a phase of renewable expansion into a phase of system integration and industrial alignment. Energy is no longer developing as an isolated sector, but as the core infrastructure layer underpinning Chile’s broader economic transformation. Mining, hydrogen, electrification, urbanisation and digital infrastructure are no longer parallel trends; they are increasingly interdependent components of a single integrated energy-industrial system.

Ultimately, the success of Chile’s energy transition will not be measured by installed renewable capacity or project announcements, but by the country’s ability to convert its exceptional natural resource base into sustained industrial competitiveness, export resilience and long-term economic value. In this context, Chile is emerging not simply as a renewable energy leader, but as one of the first examples of a fully integrated energy-industrial economy, where system design — rather than resource availability — determines the trajectory of national competitiveness.

Author: Derek Michalski, Editor