Author: Derek Michalski, Editor, The Voice of Renewables

Spain has emerged as one of Europe’s most ambitious hydrogen markets. Supported by some of the continent’s strongest solar and wind resources, extensive industrial demand, favourable geography and significant public funding, the country has positioned itself at the centre of Europe’s hydrogen ambitions. Yet despite billions of euros of announced investment and a growing pipeline of projects, Spain’s hydrogen sector has entered a critical new phase. The key challenge is no longer technological feasibility. Electrolysers are commercially available, renewable electricity is abundant and industrial applications are well understood. The question now is whether regulation can create a sufficiently bankable market to support large-scale deployment.

Over the past five years, Spain’s hydrogen sector has largely been driven by policy ambition. The publication of the Hydrogen Roadmap, the emergence of the European Green Deal, the REPowerEU strategy and successive funding programmes created momentum across the industry. Today, however, investors are increasingly focused on regulation rather than strategy. The future success of Spain’s hydrogen economy will depend upon the implementation of RED III, the EU Hydrogen and Decarbonised Gas Package, RFNBO certification requirements, hydrogen network regulation, transport infrastructure and demand-side obligations. In many respects, Spain has already solved the supply-side challenge. The remaining task is to establish the commercial framework that allows projects to move from announcement to construction and operation.

This transition is reflected in comments from industry leaders. Arturo Gonzalo, Chief Executive of Enagás, has repeatedly stressed the need for “visibility as soon as possible on the regulatory framework” and for “supportive policy” to enable investment decisions. These remarks are particularly significant because they illustrate how the industry’s priorities have changed. Five years ago, hydrogen discussions focused primarily on technology and costs. Today, the central concern is regulatory certainty. Investors need clarity regarding certification rules, transport tariffs, infrastructure access and future demand before committing billions of euros to projects with investment horizons extending several decades.

At the centre of Spain’s regulatory landscape is the European framework governing Renewable Fuels of Non-Biological Origin, or RFNBOs. While often discussed as a technical compliance issue, RFNBO regulation has become one of the most important commercial considerations in the market. A hydrogen project may be technically capable of producing renewable hydrogen, but unless it satisfies RFNBO requirements, it may struggle to access subsidies, premium markets or regulatory compliance mechanisms. For developers and lenders alike, RFNBO compliance is increasingly viewed as a prerequisite for project finance.

The RFNBO framework is built around three principles: additionality, geographic correlation and temporal correlation. Additionality requires hydrogen producers to demonstrate that the renewable electricity used for electrolysis is sourced from new renewable generation assets rather than existing capacity. Geographic correlation requires renewable electricity generation and hydrogen production to occur within specified geographical boundaries. Temporal correlation requires hydrogen production to align with renewable electricity generation over defined time periods, with regulations moving progressively towards tighter matching requirements. These rules were introduced to ensure environmental integrity and prevent renewable hydrogen production from simply diverting existing renewable electricity away from consumers. However, they also create substantial commercial challenges. Electrolysers achieve the strongest economics when operating at high utilisation rates. Stricter temporal matching requirements can reduce operating hours, increase production costs and complicate project financing. As a result, many developers now view certification risk as equally important as technology risk.

The implementation of RED III is therefore central to Spain’s hydrogen future. While the legislation creates future demand through renewable fuel targets and industrial decarbonisation requirements, it also establishes the compliance framework that will determine which projects qualify as renewable. For many developers, the economics of a project are no longer determined primarily by electrolyser efficiency or renewable electricity prices, but by the ability to achieve and maintain RFNBO certification. The distinction may appear administrative, but it has become one of the most important drivers of project bankability across Europe.

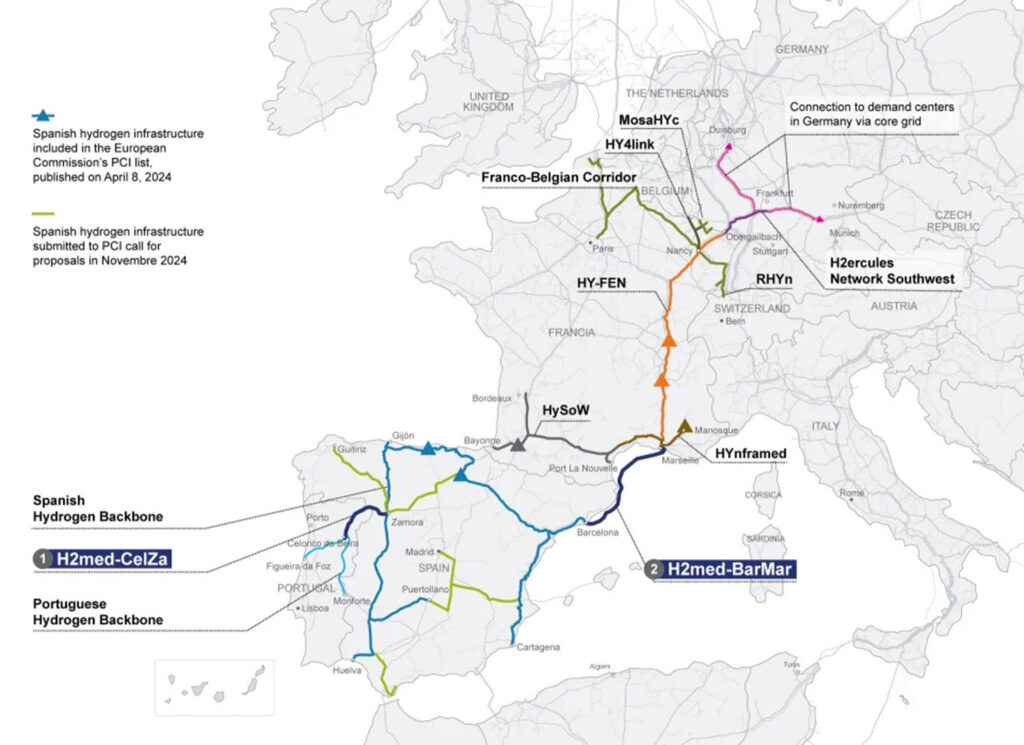

Alongside certification, infrastructure has emerged as another critical component of Spain’s hydrogen strategy. Hydrogen production alone does not create a market. Infrastructure creates markets. This reality explains why Enagás occupies such a pivotal position within Spain’s hydrogen sector. The company is leading development of the Spanish Hydrogen Backbone, a proposed network of approximately 2,600 kilometres of dedicated hydrogen pipelines designed to connect production centres, industrial clusters, storage facilities and export corridors. The network is intended to form the foundation of Spain’s future hydrogen economy while linking the country to broader European markets.

The significance of this infrastructure extends far beyond domestic demand. Spain’s hydrogen ambitions are fundamentally linked to exports. The country’s renewable resources are capable of supporting hydrogen production volumes that may ultimately exceed domestic consumption. Consequently, access to export markets is central to the commercial viability of many planned projects. This is where H2Med becomes particularly important. The flagship corridor linking Spain, Portugal and France is designed to connect Iberian hydrogen production with demand centres in Northern Europe. Gonzalo has described Andalusia as possessing “extraordinary potential to help Spain become the great European green hydrogen hub”. This statement reflects a strategic assumption underpinning Spain’s hydrogen policy: the country is not merely attempting to decarbonise its own economy but is seeking to become a major supplier of renewable molecules to Europe.

The importance of H2Med cannot be overstated. Germany, the Netherlands and Belgium are expected to become significant hydrogen importers as they pursue decarbonisation targets while facing constraints on domestic renewable generation. Spain’s ability to access these markets could ultimately determine the success of its hydrogen strategy. Without export infrastructure, many planned projects risk becoming dependent upon a relatively limited domestic market. With H2Med, Spain gains access to some of Europe’s largest future hydrogen consumers.

Yet infrastructure alone is insufficient. The regulatory framework governing hydrogen transportation remains under development, and this may prove one of the most consequential areas of policy over the next several years. Investors require clarity regarding how hydrogen networks will operate, how costs will be recovered and how tariffs will be structured. These questions are not merely technical. They directly influence project economics and financing decisions. The hydrogen sector is effectively entering the same debates that shaped Europe’s gas transmission system decades ago. Questions surrounding regulated asset bases, entry-exit tariffs, capacity allocation mechanisms and third-party access will ultimately determine whether infrastructure investment can proceed at the required scale.

The implementation of the EU Hydrogen and Decarbonised Gas Package is therefore attracting significant attention. While less widely discussed than RED III, the package may prove equally important. It establishes the regulatory foundations of a future European hydrogen market, including dedicated hydrogen network operators, cross-border infrastructure planning, market rules and access requirements. For Spain, these regulations will determine how the Hydrogen Backbone and H2Med function commercially. In many respects, the legislation represents the birth of a regulated European hydrogen market.

Against this backdrop, several projects are emerging as critical test cases for the sector. Perhaps the most important is Moeve’s Andalusian Green Hydrogen Valley. Formerly known as Cepsa, Moeve has become one of Europe’s most aggressive hydrogen investors. In 2026, the company approved the Final Investment Decision for the first phase of its flagship project in Huelva. The Onuba development includes an initial electrolyser capacity of 300 MW, with expansion potential beyond that level, representing an investment exceeding €1 billion. Importantly, the project has secured substantial public support and is expected to supply renewable hydrogen for industrial applications, fuels and chemicals. More significant than its size, however, is the fact that the project has reached Final Investment Decision. Across Europe, numerous hydrogen projects have been announced, but relatively few have secured financing and entered construction. The Andalusian Green Hydrogen Valley therefore represents one of the clearest indicators that large-scale hydrogen deployment is beginning to move beyond the conceptual stage.

Repsol’s Cartagena project provides another important example. The company approved a 100 MW electrolyser facility designed to produce approximately 15,000 tonnes of renewable hydrogen annually. Unlike many greenfield hydrogen projects, Cartagena is anchored by existing industrial demand. Repsol already consumes substantial quantities of hydrogen within its refining operations, and the project is designed to replace grey hydrogen rather than create entirely new demand. This distinction is increasingly important. Many of the most commercially viable hydrogen projects are not creating new markets but decarbonising existing hydrogen consumption. Refining, chemicals and fertiliser production already rely heavily on hydrogen, making them natural candidates for early adoption.

The bp-Iberdrola Castellón project illustrates a similar approach. Expected to become Spain’s largest operational green hydrogen facility upon commissioning, the project will supply hydrogen to replace existing refinery demand. This reflects a broader trend visible throughout the European market. The first successful applications of renewable hydrogen are not expected to be domestic heating or passenger vehicles. Instead, they are emerging in sectors where hydrogen is already used and where decarbonisation pressures are increasing.

This distinction is particularly important when examining hydrogen’s role in industrial decarbonisation. Public discussions often focus on future applications, yet hydrogen is already widely consumed within Spanish industry. Refineries operated by Repsol, Moeve and bp use hydrogen extensively for hydrocracking and desulphurisation. The fertiliser industry relies on hydrogen as a feedstock for ammonia production. Chemical manufacturers consume hydrogen in a variety of industrial processes. The initial phase of hydrogen decarbonisation is therefore centred on replacing existing grey hydrogen with renewable alternatives rather than creating entirely new demand streams. This approach offers significant advantages. Infrastructure already exists, technical expertise is established and demand is well understood. As a result, many developers increasingly view industrial substitution as the lowest-risk pathway to commercial deployment.

Heavy transport remains a more complex proposition. Policymakers continue to identify hydrogen as a potential solution for long-haul trucking, shipping and aviation, particularly where battery-electric alternatives face limitations. However, deployment remains at a relatively early stage. Hydrogen fuel-cell trucks offer advantages including rapid refuelling, long range and high payload capacity, yet costs remain high and fuelling infrastructure is limited. Consequently, most heavy transport initiatives in Spain remain pilot projects rather than large-scale commercial operations.

The maritime sector may ultimately present a stronger opportunity. Spain’s major ports, including Algeciras, Huelva, Valencia and Bilbao, are increasingly examining hydrogen-derived fuels such as green ammonia and e-methanol as pathways towards decarbonisation. Maritime transport is particularly well suited to synthetic fuels because of its energy requirements and operational patterns. As international regulations tighten, hydrogen-derived maritime fuels are expected to become an increasingly important source of demand.

Aviation represents another emerging market. Sustainable Aviation Fuel mandates introduced at European level are expected to drive growing interest in synthetic fuels produced using renewable hydrogen. Several major Spanish hydrogen projects explicitly identify aviation fuels as a target market. Over the longer term, this could create a substantial new source of demand beyond traditional industrial applications.

Despite these opportunities, the greatest challenge facing Spain’s hydrogen sector remains demand creation. The industry increasingly faces a paradox. Announced production capacity already exceeds current consumption requirements, yet many projects continue to struggle to secure long-term offtake agreements. The problem is not supply. It is demand. This is why regulatory measures such as RED III are so important. Industrial mandates, transport obligations, sustainable fuel requirements and carbon pricing mechanisms will all play a crucial role in creating the demand needed to support investment. Without such measures, hydrogen risks remaining dependent upon subsidies and demonstration projects.

Spain therefore finds itself at a pivotal moment. Few countries possess such a favourable combination of renewable resources, industrial demand, infrastructure plans and political support. The country has established itself as one of Europe’s most important hydrogen markets and is well positioned to become a leading producer of renewable hydrogen. Yet the next phase of development will be determined less by engineering and more by regulation. The technology exists. Capital is available. Major companies have committed investment. What remains is the creation of a stable regulatory framework capable of transforming ambition into commercial reality.

The industry’s message is increasingly consistent. As Enagás and other market participants have argued, regulatory certainty is now the critical requirement. The future of Spain’s hydrogen economy will not be determined by whether hydrogen can be produced. It will be determined by whether policymakers can create the market conditions necessary for that hydrogen to be transported, certified, sold and consumed at scale. If they succeed, Spain could become Europe’s dominant green hydrogen hub. If they fail, many of today’s ambitious projects may struggle to move beyond the planning stage.

Main image: A 50kW H2Pro electrolyser: H2Pro’s largest R&D system to date.